Sustainability – more than just a buzzword!

At CEMS, sustainability is more than just a buzzword – it's the foundation! We offer tailor-made solutions that not only help your business grow economically but do so in a way that aligns with responsibility towards the environment and the people we impact.

We see the future in sustainability The sustainability agenda is evolving rapidly – and so are we. Our dynamic platform is designed to keep pace with changing demands and regulations, ensuring your business stays ahead. Whether it's new legal requirements or market developments, you can trust CEMS to keep you updated and in compliance.

Everything in one place CEMS has the complete package. With our precise and innovative tools, we make it easy to create a customized ESG report that elevates your business to the next level. We combine in-depth analysis with user-friendly technology, making complex data easy to understand and accessible. This means you can make informed decisions that not only strengthen your bottom line but also contribute to a sustainable future.

Data-driven decisions with real impact At CEMS, our climate accounts are not just reports – they are strategic tools that give your company a deeper understanding of how you can reduce your environmental footprint. We help you make responsible, data-driven decisions that positively impact the environment and enhance your business's competitiveness. We believe that responsibility today creates a sustainable future tomorrow.

Top-notch user-friendliness From start to finish, our platform is designed to be simple and efficient for everyone – whether it’s your employees, suppliers, or auditors. Our system ensures that complex processes are made easy and manageable, so you can focus on what really matters: making a positive impact.

ESG concepts - including legislation and regulations

Introduction

When working with ESG reporting, there are many concepts to keep track of. It doesn't get easier that these concepts are intertwined and partially overlap. This is a rapidly evolving area with rules and requirements that are constantly changing, as well as rules and requirements that are still being developed.

CEMS encourages staying informed about the rules and requirements for large publicly listed companies—even if your company does not fall into this category—so that you can stay ahead of the requirements. It is not unlikely that these stringent requirements will be extended to smaller companies as well. Additionally, it’s a good idea to be proactive so you can provide information that your partners may request.

The following introduction provides a brief overview of some of the key concepts and regulations within the ESG field:

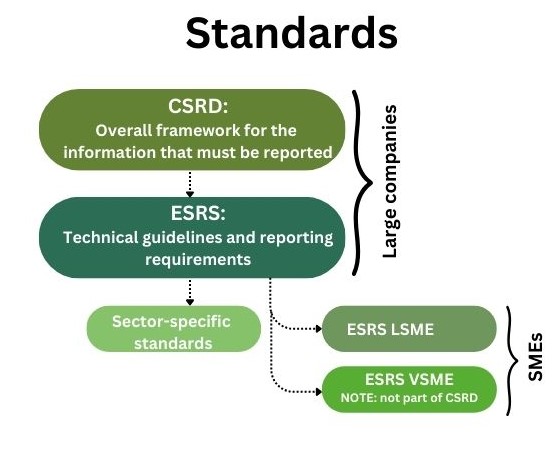

- CSRD (Corporate Sustainability Reporting Directive)

- ESRS (European Sustainability Reporting Standards)

- Including sector-specific ESRS requirements as well as ESRS VSME and ESRS LSME.

- CS3D (also known as CSDDD) (Corporate Sustainability Due Diligence Directive)

- EU Taxonomy for Sustainable Activities

A fundamental understanding of these concepts will help you navigate ESG reporting and be prepared for future requirements. You will be well-equipped to understand the context of the following sections and explanations of terms.

However, we will start with a brief presentation of EFRAG, along with a short definition of large companies and small and medium-sized enterprises (SMEs).

EFRAG

EFRAG (European Financial Reporting Advisory Group) is a private association, established in 2001 with the support of the European Commission.

In 2022, EFRAG expanded its role under the CSRD and now provides technical advice to the Commission by developing draft EU standards for sustainability reporting. They have played a central role in the development of the ESRS requirements.

EFRAG serves as an umbrella organization for the CSRD and ESRS. EFRAG develops sustainability reporting standards that help companies meet the requirements of the CSRD. Through the ESRS, EFRAG ensures consistent guidelines for sustainability reporting in the EU, promoting transparency and comparability.

Large Companies & SMEs

Large companies are defined as those with 250 or more full-time employees (FTEs) or an annual revenue exceeding 50 million euros or a balance sheet total exceeding 43 million euros.

Small and medium-sized enterprises (SMEs) are a category of businesses defined as having fewer than 250 full-time employees (FTEs) and an annual revenue of up to 50 million euros or a balance sheet total of up to 43 million euros.

ESG legislation

CSRD (Corporate Sustainability Reporting Directive) is an EU legislation that requires companies to report on their sustainability activities, such as environmental impact and social conditions. It expands previous regulations, so that more companies are now required to report.

For large companies—particularly publicly listed companies and those with over 250 employees, a turnover exceeding 40 million euros, or a balance sheet total exceeding 20 million euros—the reporting requirements are extensive and detailed. The CSRD expands previous regulations, so that more companies are now required to report, and the requirements gradually apply to more types of companies.

For SMEs, the requirements under the CSRD are more lenient. This point will be elaborated on later.

ESRS (European Sustainability Reporting Standards) are the standards that companies must follow when reporting under the CSRD. They specify exactly what information must be included in the reports, such as on climate, social conditions, and governance.

CS3D (Corporate Sustainability Due Diligence Directive) requires that companies not only report on sustainability but also actively take responsibility for human rights and environmental impacts throughout their value chain, including suppliers.

ESRS is divided into two main categories:

- Cross-cutting standards: Cover overarching topics such as governance, strategy, and risk management.

- Topic-specific standards: Cover specific areas such as climate, social conditions, and the environment, and are tailored to the company's size and sector

Additionally, sector-specific ESRS requirements are on the way. These sector-specific ESRS requirements are future reporting standards that will be developed to address the specific sustainability challenges and opportunities present in various sectors. The sectors include:

- Oil and water

- Coal, quarrying, and mining

- Road transport

- Textiles, accessories, footwear, and jewelry

- Financial institutions

- Agriculture and fishing

- Motor vehicles

- Energy production and utilities

- Food and beverages

For small and medium-sized enterprises, the requirements under the CSRD are less stringent and less extensive.

ESRS VSME (Voluntary Reporting Standard for SMEs) is a simplified version of the ESRS requirements, specifically designed for small and medium-sized enterprises to make it easier for them to meet the standards' requirements. ESRS VSME is currently voluntary to follow.

ESRS VSME falls outside the mandate of the CSRD and is driven by the market's need for a voluntary sustainability reporting standard for non-listed SMEs and micro-enterprises, aimed at helping them meet ESG requirements from banks or partners in their value chain.

Currently, work is being done on:

- Basic module with 12 overarching disclosure points.

- Narrative module with 5 overarching disclosure points.

- Business partner module based on the SMEs' business partners. Note that a double materiality assessment must be conducted to comply with the rules for expanding the module.

In addition, ESRS standards for publicly listed SMEs are being developed. These are called ESRS LSME.

ESRS LSME (ESRS for Listed SMEs) stems from the CSRD, which mandates EFRAG to develop a simplified standard for publicly listed SMEs, small banks, and captive insurance companies. It is an exception to the sector-independent ESRS and will be adopted as a delegated act by the European Commission.

Overall, the CSRD and ESRS require reporting, while the CS3D goes a step further by demanding action and accountability in the value chain.

The EU taxonomy is connected to the CSRD, ESRS, and CS3D because it helps companies meet their reporting requirements. Under the CSRD, companies must report on their sustainability, and the taxonomy indicates what is considered sustainable. The ESRS explains how the reporting should be done, while the CS3D requires companies to ensure sustainability throughout the value chain, also utilizing the taxonomy.

The EU Taxonomy is a common classification system that defines which economic activities can be considered sustainable. It serves as a guide for companies to identify and report their environmentally friendly activities.

Sources: EFRAG and Virksomhedsguiden.

September 2024 version 3.

Emission calculator

The ESG space is constantly evolving, and at CEMS, we understand that ESG reporting can seem overwhelming at first. We encourage you to consider your first ESG report as a learning experience – we all evolve along the way. Even uncertain or inaccurate reporting is better than no reporting, and the process gets easier with each year.

Below, we present some of the more complex concepts that you will encounter in our emission and reduction concepts.

Fuel in own vehicles:

Fuel consumption in own vehicles always has this text first. Subsequently, the type of fuel in question is specified. Here, the publicly available source is used as a reference.

Consumption of other transport:

Consumption of other transport always has this text first. Subsequently, the type of fuel, the mode of transport (goods transport, employee transport or employee cars) and the relevant source are specified. Publicly available sources are used as a reference.

Emission reference, for fuel in own vehicles + consumption of other transport:

To determine the CO₂e emissions of the fuel type you have purchased, you must contact your supplier and obtain their emissions reference. This reference indicates the CO₂e emissions of the product.

Supplier Scope 1, 2 or 3 emssion data:

To determine the CO₂e emissions of the product you have purchased, you must contact your supplier and obtain their emissions reference. This reference indicates the CO₂e emissions of the product.

Consumption from own plants:

Consumption from own plants always has this text first. Subsequently, specify the fuel unit used. Publicly available sources are used as a reference.

Clitoris:

All units are documented with publicly available sources, except for emission references and supplier emissions data.

Total Purchases:

For total purchases (several invoices in the period), where the supplier does not have emission data for the product quantity, and where the invoice includes both product purchases, freight and man-hours (purchases, products and services), the following units are used when entering: Purchases, products and services – services and services.

Example: Cleaning (Purchasing, products and services – services and services). It is a publicly available source reference that can deal with product purchases, freight and man-hours.

Quantities:

Where possible, it is always best and most correct to use units in quantities, as quantities are not variable, unlike emissions that are calculated in currency – as currency is variable and will not give the actual correct emission figure.

Can you save money by using CEMS?

If you, as a user, register CO2e reductions that your auditor approves, this can be done through the user's accounts, where you can gain deductions for compensation.

The value of compensation can vary and depends on several factors, including the amount of registered CO2e reductions and the applicable tax regulations. We recommend consulting your auditor or tax expert for specific information on how to take advantage of these deduction opportunities.

Please note that cash payments directly from CEMS are not possible. CEMS functions as a platform for registering and documenting CO2e reductions and offers a transparent process for compensation.

What is online accreditation?

What is online accreditation?

Introduction to Efficient Business Practices

Online accreditation represents an innovative approach to the business world, where CEMS facilitates and your auditor approves a digital accreditation process. This advanced system is designed to optimize and streamline the verification process by bringing it into the digital era.

Accreditation with CEMS:

CEMS is a platform that accredits CO2 equivalents online, enabling an efficient and digital approval process for businesses and organizations. By integrating technology and expertise, CEMS offers a platform that creates a seamless documentation and accreditation experience for organizations and businesses.

Auditor Approval:

An essential dimension of online accreditation is approval from your company's auditor. This process ensures that accreditation standards are met and that the company's practices adhere to the necessary criteria. Thus, auditing plays a central role in confirming the accuracy and credibility of the online accreditation process.

Benefits of online accreditation:

- Efficiency: Digital accreditation reduces the time and resources typically required by traditional methods.

- Transparency: The digital process provides full transparency and traceability throughout the accreditation process.

- Auditor Validity: Approval from your auditor adds an extra layer of credibility and ensures compliance with standards.

What this means for your business:

By integrating online accreditation with CEMS and auditor approval, your company positions itself as a proactive participant in the digital transformation of business practices. This not only optimizes your processes but also enhances your company's reputation by demonstrating commitment to quality and compliance with industry standards.

What is internal climate compensation?

Internal climate compensation: Sustainability in the company's DNA

What is internal climate compensation? Internal climate compensation refers to a company's own measures and initiatives to reduce or offset its internal greenhouse gas emissions. This involves supporting projects or implementing measures that directly contribute to reducing the overall amount of CO2e or other greenhouse gases that the company generates.

Sustainable business principles: In a time where companies face increasing demands for sustainability, internal climate compensation constitutes a fundamental part of a company's DNA. It involves proactively identifying and implementing solutions that reduce the economic impact and promote a green business model.

Integration in accounts: Companies can incorporate internal climate compensation into their accounts by documenting and communicating their sustainability efforts. This step not only demonstrates accounting responsibility but also positions the company as a leader in sustainable business practices.

Benefits of internal climate compensation:

- Environmental protection: Reduce the company's internal climate footprint and contribute to environmental protection.

- Sustainable image: Strengthen the company's reputation by demonstrating a commitment to internal climate compensation.

- Accountability: Incorporate internal climate compensation into the accounts to demonstrate the company's dedication to sustainability.

We encourage companies to embrace the concept of internal climate compensation as a crucial driver for a sustainable future. By implementing internal initiatives, companies can actively contribute to a more sustainable and environmentally friendly business practice.

Can you sell an overcompensation?

Yes, you can sell an overcompensation, provided it is approved by the auditor and thus can be sold. Overcompensation has a market value, which it can be traded for. The market value is variable and is approximately 1,500 DKK per ton.

See link from Klimarådet's (The Danish Council on Climate Change Secretariat) webpage: https://klimaraadet.dk/da/virkemiddel/co2-pris-i-offentlige-projekter-konsistent-med-70-procentsmaalet

CEMS can generate a digital certificate that the user can utilize to sell their accredited CO2e savings. There's a small fee to CEMS for using this model.

How are users added on CEMS?

Under User Management, the admin can add a new user. The admin can grant admin rights, create rights, and approve rights to a user. A new user will receive an email with a code, and then the user is ready to go.

What are page versions?

Updates to versions are available at the bottom of our calculation tools. Each time a new version is uploaded, the version number changes automatically, allowing you to track the changes over time and take advantage of the latest updates.

What is an SME?

SME stands for "Small and Medium-sized Enterprises."

It is a category of businesses defined by specific criteria regarding the number of employees, revenue, and total assets.

The Importance of SMEs in Business

For business owners, it is essential to determine if their company falls under the SME category. Why? There are various financing and support schemes specifically targeted at SMEs based on the EU's definition. Additionally, accounting rules and documentation requirements can vary depending on whether a company is classified as an SME.

EU's Definition of SMEs

The EU differentiates companies based on their size, including the number of employees, revenue, and total assets.

In summary, according to the EU, SMEs are defined as companies that fall within the categories of small and medium-sized enterprises. This means they typically have between 10 and 249 employees, and their revenue or total assets range between €10-50 million.

Link to SME Denmark website: SME Denmark

Consulting Services

If you would like a meeting with a consultant who can assist you in getting started with the use of CEMS and potentially provide advice and guidance in CO2e emissions or reduction, LCA calculation, or ESG reporting, please contact us for a discussion. You can purchase the consultancy service on the Webshop under products.

What is climate accounting?

Climate ESG Monitoring Systems (CEMS) is designed to calculate the climate impact, including CO2 equivalents (CO2e), enabling the user to compute the necessary data for the preparation of a climate account. CO2e is a metric unit that combines all greenhouse gas emissions into a common measurement based on their global warming potential.

CEMS, measuring CO2e emissions, is crucial for companies and organizations looking to quantify and report their contributions to climate change. This is a key component of sustainability reporting and part of efforts to reduce overall climate impact.

A climate account, also known as an environmental account or sustainability report, is a method for quantifying and reporting an entity's or organization's total climate impact and environmental footprint. The purpose of a climate account is to provide a detailed picture of the greenhouse gas emissions originating from various activities or processes within a given timeframe.

A typical climate account includes measuring and reporting emissions from sources such as:

-

Direct emissions (Scope 1): This includes direct emissions from the company's own activities, such as fuel use in production processes and transportation.

-

Indirect energy-related emissions (Scope 2): This covers indirect emissions from externally purchased electricity, steam, or heat.

-

Other indirect emissions (Scope 3): This includes all other indirect emissions, such as suppliers' activities, transportation of goods, waste, employee commuting, purchased goods and services, and end-use of products.

The purpose of a climate account is not only to report emissions but also to identify opportunities for reduction and sustainability improvement. It helps organizations understand their environmental impact and make informed decisions to reduce their climate impact over time. Climate accounts are an important part of businesses' and society's efforts to move towards more sustainable and climate-friendly practices.

The process of reducing CO2e emissions can involve several measures, such as:

-

Energy efficiency: Implementing energy-efficient technologies and practices to reduce direct and indirect energy-related emissions.

-

Renewable energy: Increased use of renewable energy sources such as solar and wind energy to reduce dependence on fossil fuels.

-

Sustainable transportation: Promotion of sustainable transportation solutions, including electric vehicles or fuel-efficient vehicles, to reduce transportation-related emissions.

-

Waste reduction: Implementation of waste reduction programs and increased recycling to decrease emissions from waste management.

-

Supply chain optimization: Collaborating with suppliers to reduce emissions throughout the supply chain.

The effort to reduce CO2e emissions is a central part of businesses' and organizations' responsibility to contribute to combating climate change and meet sustainability goals.

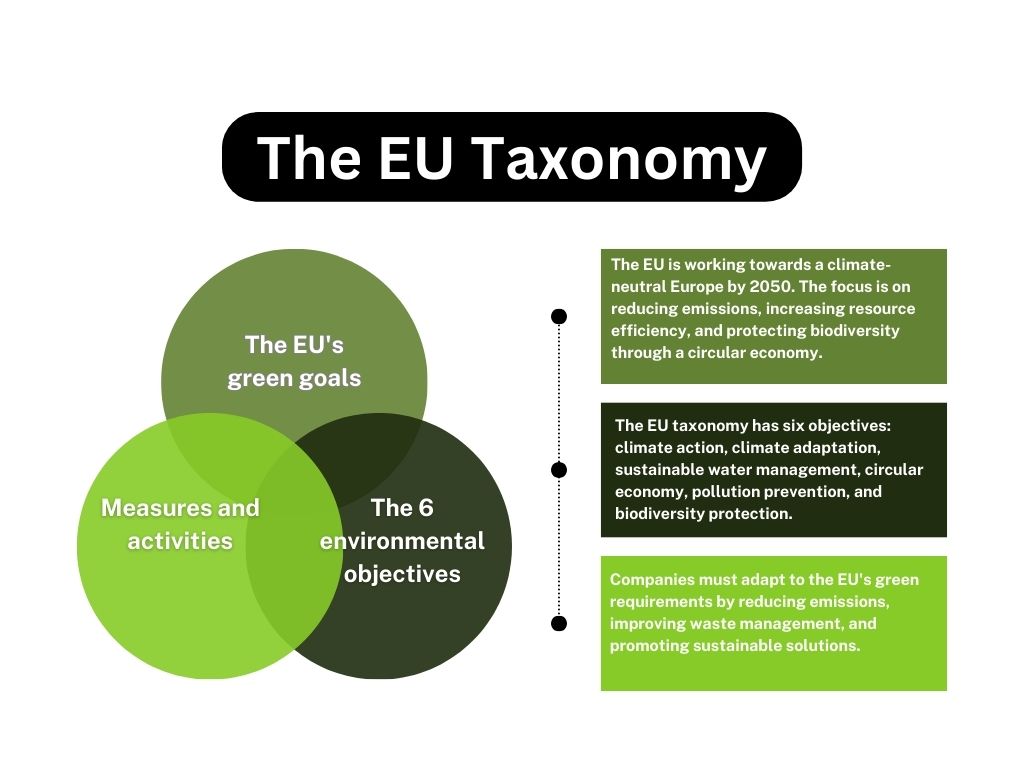

The taxonomy of the EU

The EU taxonomy is a classification system based on common definitions of sustainability. This means that when an economic activity is environmentally sustainable, it will make a significant contribution to at least one of the EU's climate and environmental goals.

The taxonomy introduces the following key elements for companies and financial institutions:

- Six environmental objectives that economic activities must substantially contribute to in order to be classified as sustainable.

- Four conditions that must be met to define whether an economic activity is sustainable.

- For each of the six environmental objectives, technical screening criteria are established, specifying conditions for all economic activities and determining whether the nine activities of the Danish Standards Foundation constitute a significant contribution to an environmental objective and do not harm the other environmental objectives. These minimum conditions must be met and documented for an economic activity to be considered environmentally sustainable.

- Mandatory reporting requirements for companies, which among other things, must disclose the proportion of their revenue generated within business areas that are sustainable according to the taxonomy.

- Mandatory reporting requirements for financial institutions, which must disclose the proportion of their total investments that are sustainable according to the taxonomy.

The taxonomy of the EU thus translates the EU's climate and environmental goals into a set of criteria that determine when an economic activity is considered environmentally sustainable

An economic activity is defined as goods or services offered on a market. For example, construction is an economic activity for a company. The execution of the construction project involves economic activities that include both physical goods, such as windows, and services such as consulting.

Companies can use the taxonomy's classification to showcase and communicate their sustainable initiatives, while investors can use the taxonomy to find companies to invest in that can demonstrate they are engaged in sustainable practices.

If you want to read the EU taxonomy regulation, see:

(EU) 2020/852.

Source: Dansk Standard

CSRD and ESG: An industry-specific overview of reporting requirements

A Comprehensive Overview of Key Aspects Across Industries

What are DEFRA & the GHG Protocol?

What are DEFRA & the GHG Protocol?

DEFRA is a set of conversion factors that allow organizations and individuals to calculate greenhouse gas emissions (GHG) from a range of activities, including energy consumption, water use, waste disposal, recycling, and transportation activities.

https://ghgprotocol.org/Third-Party-Databases/Defra

DEFRA stands for the Department for Environment, Food & Rural Affairs, and it is a UK government department focusing on the environment, food production, agriculture, and rural affairs. DEFRA plays a role in the development and implementation of policies related to environmental protection, sustainability, and climate in the United Kingdom.

https://ghgprotocol.org/about-us

What is GHG Protocol?

GHG Protocol establishes comprehensive global standardized frameworks to measure and manage greenhouse gas (GHG) emissions from private and public sector operations, value chains and mitigation actions.

Building on a 20-year partnership between World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), GHG Protocol works with governments, industry associations, NGOs, businesses and other organizations.

History of GHG Protocol

GHG Protocol arose when WRI and WBCSD recognized the need for an international standard for corporate GHG accounting and reporting in the late 1990s. Together with large corporate partners such as BP and General Motors, in 1998 WRI published a report called, “Safe Climate, Sound Business.” It identified an action agenda to address climate change that included the need for standardized measurement of GHG emissions.

Source: https://ghgprotocol.org/about-us

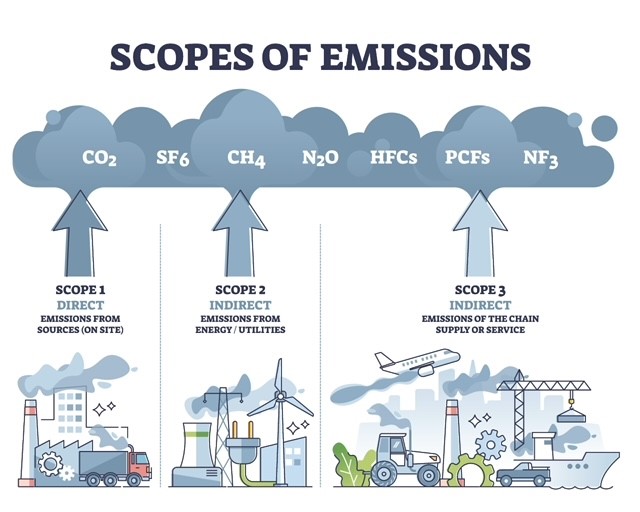

What are Scope 1, Scope 2, and Scope 3?

What is the Greenhouse Gas Protocol? - Scope 1, Scope 2, and Scope 3

According to the most recognized emissions calculation method, called the Greenhouse Gas Protocol (GhG Protocol), companies should categorize their emissions into three scopes. Calculations conducted in accordance with the GhG Protocol can be seen as an inventory of CO2 emissions to understand which business activities have the greatest impact.

Scope 1: Covers direct emissions from the company and includes, among other things, mobile and stationary fuel combustion, and emissions from industrial processes. These emissions are related to buildings, vehicles, and stationary engines operated by the company.

Scope 2: This involves indirect emissions from the purchase of energy generated outside the reporting company's operations, such as electricity, heat, cooling systems using gas, and steam. These are areas that the company consumes and can control, but does not own or produce itself.

Scope 3: This scope includes indirect emissions divided into 15 categories. Scope 3 will typically cover 75-95% of a company's total emissions. The 15 categories in Scope 3 aim to provide companies with a systematic framework for measuring, tracking, and reducing emissions across the value chain. The categories are disaggregated to avoid overlap, ensuring that double counting of Scope 3 emissions is avoided for each company. Scope 3 emissions are associated with both upstream and downstream activities in the value chain.

Below are the Scope 3 categories in order. Here are some examples of activities included in each category and should be counted as emissions in Scope 3 (these should not be considered Scope 1 or 2 emissions).

1. Purchase of goods and services:

- Procurement of office supplies, cafeteria food, goods sold to end-users, or materials for production such as wood.

- Procurement of data storage, cleaning services, and other services.

2. Capital goods:

- Procurement of equipment, machinery, buildings, facilities and vehicles used to manufacture goods or provide a service.

3. Fuel and energy-related activities:

- Extraction of coal

- Refining of gasoline

- Transmission and distribution of natural gas

- Production of purchased electricity

4. Upstream transport and distribution:

- All purchased transport and distribution services.

- Transport of purchased goods from 1st tier suppliers.

5. Waste:

- Waste generated in daily operations, such as organic waste, ordinary waste, plastic etc. In addition, it includes emssions from treatment, which relates to whether waste is recycled, incinerated or landfilled.

- Operational wastewater.

6. Business trip:

- Distance traveled by employees in various means of transport such as plane, taxi, train etc. for business purposes.

7. Employee commuting:

- Distance traveled by employees between work and home by bicycle, public transport, car etc.

8. Upstream leased assets:

- Leased office spaces or leased company cars

9. Downstream transport and distribution:

- Commuting customers to and from the reporting companies' stores.

- Last mile delivery purchased by customers.

10. Processing of sold products:

- Processing of glass (intermediate product) for the production of wine bottles (end product).

11. Use of sold products:

- Electricity consumption of sold electronics over their expected lifespan.

- Fuel consumption of vehicles sold over their expected lifespan.

12. Final processing of sold products:

- Final processing of the product, e.g. the glass container is recycled, whereas the plastic label goes to incineration.

13. Downstream leased assets:

- Energy consumption in buildings rented out to other companies.

- Fuel consumption of vehicles leased to other companies.

14. Franchising:

- The franchisor, the organization issuing the license, should report Scope 1 and Scope 2 emissions from franchisees.

15. Investments:

- If the company has invested 10% in a company, this company is responsible for 10% of the company's emissions.

- Financial institutions must also include emissions from commercial loans, mortgage loans, project financing, etc.

There is a significant interest among companies in addressing their Scope 3 emissions, as they constitute a large portion of a company's emissions. However, it makes sense to calculate Scope 1 and 2 before delving into Scope 3, as Scope 3 calculations often require more effort and can be more complex. Once the company has a handle on emissions in Scope 1 and 2, there are some steps that can help the company get started with calculating Scope 3:

● Understand the key emissions in scope 3: Start by reviewing each Scope 3 category in the GhG protocol. Understand which emissions are related to the company's operations and write them down.

● Create a prioritization list: Categories should be ranked to understand their impact. It is preferred to rank the categories by making a rough estimate of their CO2 emissions, using a spend-based method or an estimation of purchased quantities/units multiplied by CO2 coefficients. There are free online calculation tools available that can be used for estimation, such as The Climate Compass. However, it should be noted that these tools can only be used as indicative of the level of your company's emissions.

Once you have an estimation, you can rank the categories by percentage of the company's CO2 emissions. In case you are not familiar with this, the categories can also be evaluated based on several other parameters to understand their significance; for example, the quantity of purchased units, the impact it has on operations, the risk it poses, or the categories with the highest expenditures. Knowing which are the largest or most important categories can aid the process in selecting those that are easiest to start with. You want this process to result in a priority list that balances the impact of emissions and the feasibility of collecting data.

● Choose a method for data collection: Each category in Scope 3 may require different data collection methods. The method you choose depends on the availability of data as well as the desired quality and accuracy. Generally, you would choose an activity-based approach if you want higher quality and more precise accounting, whereas spend-based data is more of an estimate but also easier to handle and collect. The decision should be based on the timeframe for data collection and how many categories you wish to cover.

● Make a plan: Once you have a clear picture of your categories, decide whether you want to focus on the largest category first or go for the low-hanging fruit. The general recommendation would be to focus on one or a few categories at a time and create a plan for which categories you will include in the next report. For banks, it may make sense to exclusively focus on category 15, investments, as this can account for well over 90% of the company's emissions. However, if the largest category requires extensive work and there is limited time for data collection, it may make sense to start with some smaller and easier categories. Even though the bank's smaller categories may only cover 10% of the emissions, it will be an opportunity to learn how to approach different types of calculations for next year's reporting and therefore also be a good start. Attempting to do everything at once can result in poor-quality data or overwhelming work.

● Transparent reporting: If you don't have all the necessary data or there is uncertainty about the collected data, it's best to make notes and tell the truth. It's okay if you use spend-based reporting or if you can only collect data on some of your purchased products and services. However, you should be honest in your reporting about this and let the readers know the extent and quality of the collected data.

Souce: Dansk Industri (Confederation of Danish Industry)

What is CEMS Data Scope?

CEMS has built Data Scope for everything that does not have an emission, but still needs to be reported on.

That is, everything that lies under S and G.

The Data Scope points are located under the emission calculator and documentation can be uploaded.

When you upload documentation on a point, you get a green star. If you upload more than one document as documentation on point, you will get a yellow star. If you do not upload documentation at one point, you get a red star.

All these documents are sent over for audit by the Auditor.

What is the GLEC Framework?

What is the GLEC Framework?

GLEC Framework: a universal method for logistics emissions accounting

In October 2019, the Smart Freight Center released the GLEC Framework, a guide for shippers, carriers and logistics service providers on how to report emissions from logistics operations. It is meant to be used in conjunction with the Corporate Standard, and it has earned the “Built on GHG Protocol” mark for its compliance with GHG Protocol’s requirements.

Freight transport forms the backbone of today's global economy. Forward-thinking companies aim to control greenhouse gas (GHG) emissions from their logistics supply chain not only because it is expected by customers, governments and investors but also because they recognize the business case of carbon accounting and reduction. Until now, comparing emissions across different modes of transport could be like comparing apples to oranges because so many methodologies exist.

The Global Logistics Emissions Council (GLEC), led by Smart Freight Centre, is a group of companies, associations and programs, and backed by leading experts and other stakeholders. It’s members include well-known companies such as DHL, SNCF, Maersk, TNT, Hapag-Lloyd, & Kuehne + Nagel. Since its inception in 2014, GLEC developed a universal method for calculating logistics emissions across road, rail, air, sea, inland waterways and transhipment centers. The “GLEC Framework for Logistics Emissions Methodologies” combines existing methods into one framework and fills the gaps.

This industry-focused guidance document is designed to work in conjunction with the voluntary GHG Protocol Corporate Accounting and Reporting Standard.

The framework is designed to increase transparency, giving companies with smaller footprints a competitive advantage. Companies can also use emissions data for logistics business decisions, such as selecting more fuel efficient modes, routes and carriers and identifying ways to increase efficiency and reduce costs.

As a next step, GLEC will encourage widespread adoption by businesses of the framework, and embed it in green freight programs, carbon-footprint calculation tools, and national and international standards. Work will also continue to fill remaining gaps and expand the framework with Black Carbon and air pollutants.

GLEC and the GHG Protocol invite companies to demonstrate a commitment to a more competitive and environmentally sustainable freight sector by implementing the GLEC Framework.

Source: ghgprotocol.org 2019: https://ghgprotocol.org/blog/glec-framework-universal-method-logistics-emissions-accounting

What is ISO 14083?

What is ISO 14083?

Today, the GHG Protocol serves as the basis for companies to calculate and report their greenhouse gases. The GHG Protocol, a global industry standard since the early 20th century. With the new ISO 142083 standard, the guidelines for describing GHG emissions from transportation chains are more specific than in the GHG Protocol. This improves the opportunities for accurately comparing GHG emissions from different transportation companies.

The first international standard for transportation chains was EN 16258, published by the European standardization body CEN in 2012. Subsequently, the EN 16258 standard formed the basis for an industry network, the Global Logistics Emissions Council (GLEC), to develop a handbook and guidance on calculating and declaring CO2 emissions from transportation and logistics services, known as the GLEC Framework. Today, the GLEC Framework is considered an industry standard (similar to the GHG Protocol), and a number of global transportation companies now cite the GLEC Framework as the standard they report according to.

The new ISO 14083 standard is in many ways an update of the two aforementioned standards.

The main principles of the new standard are:

- Calculation is based on fuel consumption and an emission factor for the fuel.

- Allocation should be based on a physical measure. For most modes of transport, this should be based on transport work, i.e., for goods, weight of goods x distance transported.

- All emissions must be included and distributed, i.e. also idling

- Calculation and reporting should include the total emissions (GHG emission total), i.e., both emissions from producing and transporting the fuel to the tank, and emissions from the vehicle (GHG emission operational).

These are the same basic principles as in the two previous standards. There are also differences:

- The new ISO 14083 standard proposes more specific principles for the allocation of GHG emissions in several areas.

- Where EN 16258 only includes emissions from the vehicles, ISO 14083 also allows for including emissions from nodes and terminals and from the energy production supplying the IT systems used in the transport sector today.

- The greenhouse effect of emissions of LNG must now be included, as must the greenhouse effect from emissions of coolant from cooling systems on the vehicles.

Globally, transportation (both passenger and freight) accounts for approximately one-quarter of total GHG emissions. With the new ISO 14083 standard, the principles for quantifying the transport sector have been clarified.

It provides a solid foundation for efforts to reduce the carbon footprint of the transport sector across transport chains and along the supply chain.

Souce: https://dasp.dk/iso-14083-ny-global-standard-for-beregning-og-deklaration-af-drivhusgasser-fra-transport-af-gods/

ISO 14001: The international standard for environmental management systems

ISO 14001 is a global standard that focuses on environmental management in companies and organizations. It was first published by the International Organization for Standardization (ISO) in 1996 and has since been updated several times to reflect changes in environmental expectations and practices.

Background and Purpose: The purpose of ISO 14001 is to provide companies with a structured foundation for establishing, implementing, maintaining, and improving their environmental management system. This includes identifying and managing environmental impacts, reducing negative environmental effects, and complying with regulatory requirements.

Elements of ISO 14001

- Environmental Management Policy: The organization develops an environmental policy committing it to comply with applicable environmental laws and improve its environmental performance.

- Planning: This step involves identifying environmental risks and opportunities as well as establishing clear objectives and action plans to achieve them.

- Implementation: The organization allocates necessary resources and competencies to meet the established environmental objectives, including employee training, procedure development, and establishment of communication channels.

- Monitoring and measurement: A key part of ISO14001 is the ability to monitor and measure environmental performance by establishing indicators that show whether targets are being met and whether adjustments are needed.

- Clarification and correction: The organization continuously reviews and evaluates its environmental management system to ensure that it is operating effectively. Any deviations or need for improvement require appropriate corrections.

- Management review: Senior management regularly reviews the organization's environmental performance, goals, and policies to ensure compliance and continuous improvement.

Benefits of ISO14001 certification

- Improved environmental performance: ISO14001 helps businesses identify and reduce their environmental impacts, which can result in less resource consumption and reduced environmental burden.

- Increased credibility: Certification demonstrates that the company takes its environmental responsibilities seriously and has established systems to manage them.

- Access to new markets: Many public institutions and businesses require their suppliers to have some form of environmental certification as a prerequisite for doing business with them.

- Reduced costs: By identifying inefficient processes or resource consumption, organizations can save money by optimizing their operations.

Challenges: While ISO14001 offers many benefits, it is not without challenges. Some point out that the standard can be too general and may not always result in concrete environmental improvements. The costs of implementation can pose a challenge for smaller businesses, and some may feel that the administrative burden is too extensive.

Conclusion: ISO14001 represents a significant standard with the potential to enhance companies' environmental performance. While it does not present a universal solution to all environmental issues, it offers a structured framework for managing and improving environmental aspects. Achieving certification requires not only dedication and resources but also underscores the company's commitment to Environmental, Social, and Governance (ESG) and Corporate Social Responsibility (CSR). Many organizations find that the benefits of ISO14001 certification extend beyond environmental improvements and include a stronger commitment to sustainability practices and an enhanced corporate image. This holistic approach to responsible corporate conduct can serve as a strategic driver for achieving sustainability goals and strengthening relationships with stakeholders, including customers, employees, and the community at large.

What are actual emissions and what are default considerations?

What is the difference between actual emissions and default/average considerations?

The difference between actual calculations of CO2 emissions and calculations based on standard values or average considerations lies in the precision and accuracy of the obtained results. Let's delve into both approaches:

- Actual calculations of CO2 emissions: With actual calculations, specific data on activities, processes, or resources contributing to CO2 emissions are collected and used. This may involve precise measurements of energy consumption, fuel usage, production processes, and other relevant parameters. Companies or organizations often conduct comprehensive analyses using data from their own operations to obtain accurate and precise figures for their CO2 emissions. This method requires more resource investment, but it results in more reliable results.

- Calculation based on default values/average considerations: In contrast, some organizations or individuals may choose to use standard values or average considerations to estimate their CO2 emissions. These standard values are often based on general assumptions or statistical averages for a given sector or activity. This method is easier and less resource-intensive, but it can also be less precise as it does not account for specific conditions in a given situation.

The benefits of actual calculations include a more accurate assessment of real impacts and opportunities to identify areas where reductions can be achieved. On the other hand, the use of standard values may be more convenient in situations where it is difficult or costly to collect specific data.

Generally speaking, the accuracy of CO2 emission calculations is crucial, especially when the goal is to make informed decisions about reducing emissions and meeting sustainability goals. Therefore, the choice between the two approaches should depend on the availability of data, resource capacity and the purpose of the calculations.

What is greenwashing?

Greenwashing - When Good Green Intentions Turn into Distorted Marketing

What is greenwashing?

Greenwashing is the practice of providing a false or misleading representation of a company's or product's environmental commitment to appear more sustainable than it actually is. This often occurs through advertising, branding, or marketing campaigns, where companies may exaggerate their sustainability initiatives or use ambiguous language to create a green image without genuine substance.

Avoid the pitfalls - Be critical, demand transparency

By understanding the phenomenon of greenwashing, consumers and businesses can navigate the complex landscape of sustainability claims more critically and ensure that they support genuine and meaningful initiatives.

Read more about greenwashing at: https://csr.dk/hvad-er-greenwashing-og-hvordan-undg%C3%A5r-du-blive-snydt

What is greenhushing?

What is greenhushing?

Greenhushing refers to situations where real and meaningful sustainability initiatives are downplayed or concealed by companies or organizations. This can occur when a company fails to market or share its genuine sustainability efforts out of fear of being accused of greenwashing or for other reasons.

Recognize the good work - Highlight true sustainability

Greenhushing calls for the need to recognize and highlight authentic sustainability initiatives. Companies that are truly making a difference should have the opportunity to share their efforts without fear of it being perceived as superficial marketing.

Read more about greenhushing at: https://www.csr.dk/hver-femte-virksomhed-beg%C3%A5r-green-hushing

What is Section 99a of the Annual Accounts Act?

According to the Annual Accounts Act § 99 a, large Danish companies must include a statement of social responsibility in their annual report. The purpose of this statement is to inform stakeholders about the company's efforts and results in areas such as the environment, social conditions and responsible business management.

Read more about the Annual Accounts Act Section 99 a at: https://danskelove.dk/%C3%A5rsregnskabsloven/99a

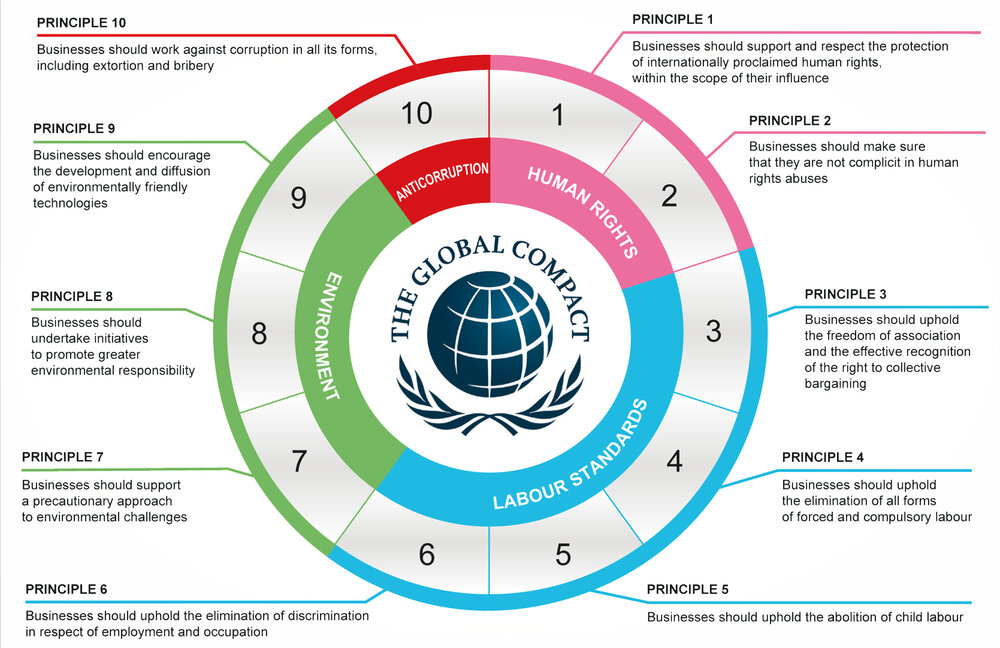

The Ten Principles of the UN Global Compact

Corporate sustainability starts with a company's value system and a principles-based approach to doing business. This means operating in ways that at least meet basic responsibilities in the areas of human rights, labor market, environment and anti-corruption. Responsible companies adopt the same values and principles wherever they are present, and know that good practice in one area does not outweigh harm in another. By incorporating The Ten Principles of the UN Global Compact into strategies, policies and procedures and establishing a culture of integrity, companies not only uphold their fundamental responsibilities to people and the planet, but also set the stage for long-term success.

The ten principles of the UN Global Compact are derived from: Universal Declaration of Human Rights , ILO Declaration on Fundamental Principles and Rights at Work , Rio Declaration on Environment and Development and United Nations Convention against Corruption.

Read more at: https://unglobalcompact.org/what-is-gc/mission/principles#

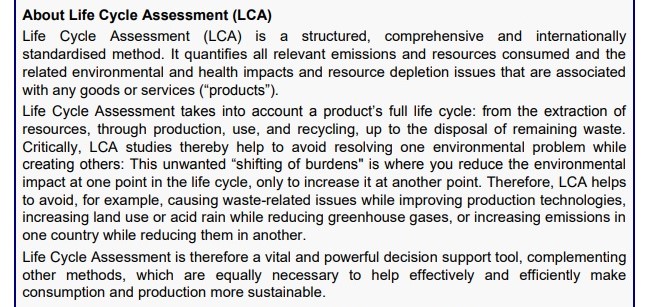

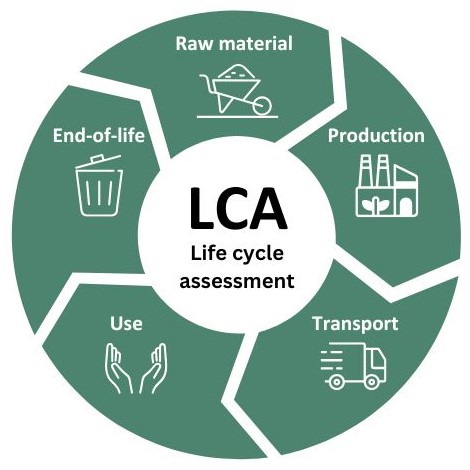

What is an LCA report?

A Life Cycle Assessment (LCA) is used to calculate the total climate footprint. Various methods and standards exist for these calculations, which can either focus solely on climate impact or include other environmental factors.

Overall, the ISO 14040 and 14044 standards serve as the cornerstones of life cycle assessments, providing an essential framework for this work.

In 2010, the European Commission published The International Reference Life Cycle Data System (ILCD) Handbook, in which an LCA is defined as follows:

In short: An LCA analyzes the entire life cycle of a product to prevent the solution to one environmental issue from creating a new problem elsewhere. It ensures a holistic perspective, where sustainable solutions provide benefits across the board.

Examples of other standards:

- ISO 14067: Carbon footprint of products

- Product Environmental Footprint (PEF): The EU's method for environmental footprinting

- DS/EN 15804: Environmental product declarations for construction products

- GHG Protocol: Standard for greenhouse gases

You can read more here:

ILCD Handbook: International Reference Life Cycle Data System (ILCD) Handbook - General guide for Life Cycle Assessment - Provisions and Action Steps (2010)

The Danish Energy Agency's Guide to Calculating Carbon Footprints

CEMS has drafts for EPD and PCR. See more here.

The Climate Compass and CEMS

The Climate Compass is a CO2 calculator developed by Erhvervsstyrelsen (The Danish Business Authority) in collaboration with Energistyrelsen (The Danish Energy Agency). The Climate Compass is a tool you can use to make informed decisions regarding climate change and sustainability. When you integrate data from the Climate Compass, it allows you to explore different scenarios, policies, and strategies to mitigate the effects of climate change through interactive tools and visualizations.

CEMS - Climate ESG Monitoring System is a unique tool that makes the use of source references from the Climate Compass easier to incorporate into an ESG report.

Sources: IPCC, NOAA, NASA, IEA, World Bank, scientific journals.

Klimakompasset

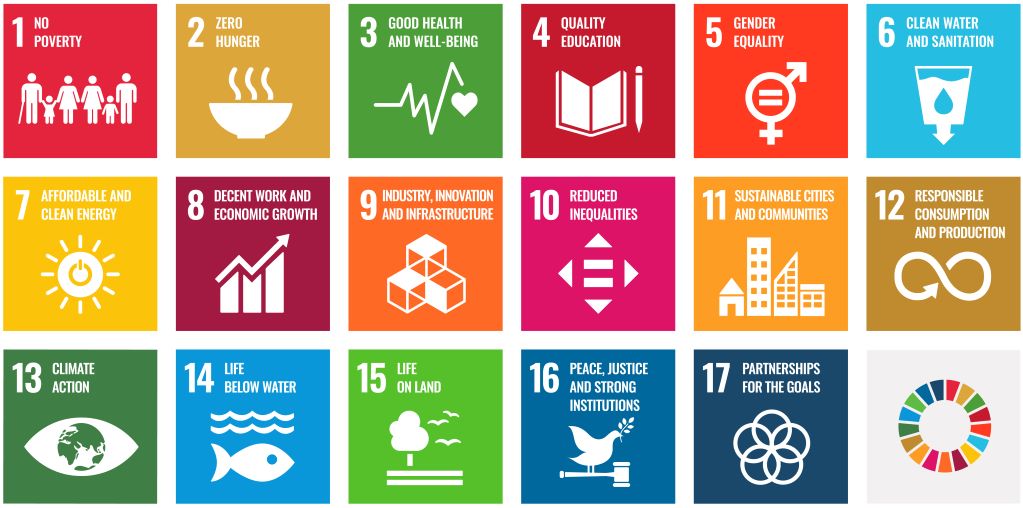

The United Nations' Sustainable Development Goals

The sustainable Development Goals (SDGs) comprise 17 concrete goals and 169 sub-goals, which commit all 193 UN member states to completely eliminate poverty and hunger in the world, reduce inequalities, ensure good education and better health for all, decent jobs and more sustainable economic growth. They also focus on promoting peace and security and strong institutions, and on strengthening international partnerships.

The SDGs thus recognise that social, economic and environmental development, peace, security and international cooperation are closely linked. Achieving sustainable development results requires a joint, global integrated effort.

And all countries must contribute. Regardless of the countries' different starting points. The major challenges we face today are global. And so are the consequences. Therefore, we need to solve challenges together.

Learn more about the goals here.

Earth Overshoot Day

Earth Overshoot Day

In this link you can read about https://overshoot.footprintnetwork.org/newsroom/country-overshoot-days/

Reference documents for your finalized ESG metrics (Data Scope)

Data Scope is a unique feature that CEMS has developed.

If you refer to an external provider a website with data or references in your finalized ESG report, you can upload this documentation in CEMS under the Emission reference (Data Scope) emission category.

As a user of CEMS, you have the option to save the reference, and in case the text or data on the website you refer to changes, you can always document what was stated when you chose to use it as a reference.

The references for S and G can be saved in CEMS Emissions Calculator (Data Scope)

The reference is saved with the date and image, along with document information. "Data Scope" can encompass a range of activities, data, or factors that do not directly fit into Scopes 1, 2, and 3 but may still be relevant to the company's sustainability practices and reporting. In general, "Data Scope" is an area where the company can include relevant information that does not fit into the traditional Scopes but is still important for providing a comprehensive overview of the company's sustainability efforts and performance.

Total number of employees FTE

FTE (Full Time Equivalent) is a term used to define the number of full-time employees in a company based on actual working hours. One full-time employee equals one FTE. A person working 50% of a full-time position equals 0.5 FTE.

The list consists of abbreviations for terms used in texts describing, among other things, ESG/CSRD and other standards.

List of abbreviations

CCAC = Climate and Clean Air Coalition

CCWG = Clean Cargo Working Group

CDP = Carbon Disclosure Project

CH4 = Methane

CNG = Compressed Natural Gas

CO2 = Carbon Dioxide

CO2e = Carbon Dioxide Equivalent

CORSIA = Carbon Offsetting and Reduction Scheme for International Aviation

COVID-19 = Coronavirus Disease 2019

CSR = Corporate Sustainability Reporting

DQA = Data Quality Assurance

DAF = Distance Adjustment Factor

DJSI = Dow Jones Sustainability Index

EC = European Commission

EEDI = Energy Efficiency Design Index

EEOI = Energy Efficiency Operational Indicator

eGRID = Emissions & Generation Resource Integrated Database

EIT = European Institute of Innovation and Technology

ERTAC = Eastern Regional Technical Advisory Committee

EU = European Union

EU ETS = European Union Emissions Trading System

FTL = Full Truck Load

GCD = Great Circle Distance

GHG = Greenhouse Gas

GIS = Geographic Information System

GLEC = Global Logistics Emissions Council

GPS = Global Positioning System

GVW = Gross Vehicle Weight

GWP = Global Warming Potential

HBEFA = HBEFA: Handbook of Emission Factors (“Emissionsfaktorhandbuch”)

HFCs = Hydrofluoro-Carbons

HFO = Heavy Fuel Oil

HGV = Heavy Goods Vehicle

HOC = Hub Operation Category

HPDI = High-Pressure Direct Injection

IATA = International Air Transport Association

ICAO = International Civil Aviation Organization

ICC = International Chamber of Commerce

ICT = Information and Communications Technology

IEA = International Energy Agency

IMO = International Maritime Organization

IPCC = Intergovernmental Panel on Climate Change

ISO = International Organization for Standardization

ITF = International Transport Forum

kg = Kilogram

KIC = Knowledge and Innovation Communities

kJ = Kilojoule

KPI = Key Performance Indicator

kWh = Kilowatt-hour

LEARN = Logistics Emissions Accounting & Reduction Network

LNG = Liquefied Natural Gas

LPG = Liquefied Petroleum Gas

LSP = Logistics Service Provider

LTL = Less than Truck Load

MDO = Marine Diesel Oil

MIT = Massachusetts Institute of Technology

N2O = Nitrous Oxide

NDCs = Nationally Determined Contributions

NF3 = Nitrogen Triflouride

NGO = Non-Government Organization

NOx = Nitrogen Oxides

NTM = Network for Transport Measures

OECD = Organization for Economic Co-operation and Development

peg = Passenger equivalent

PFCs = Perfluoro-Carbons

RAILISA = RAIL Information System and Analyses

RED2 = Renewable Energy Directive (EU)

REff Tool® = Resource Efficiency Tool

RP = Recommended Practice

SAF = SAF: Sustainable Aviation Fuel

SBTi = Science-Based Targets initiative

SDA = Sustainable Development Agenda

SDG = Sustainable Development Goals

SF6 = Sulphur Hexafluoride

SFC = Smart Freight Centre

SFD = Shortest Feasible Distance

SI engine = Spark Ignition engine

t = Tonne = 1000 kg

T&D = Transmission and Distribution

TCE = Transport Chain Element

TEU = Twenty-foot Equivalent Unit

t-km = Tonne-kilometer

TMS = Transport Management System

TOC = Transport Operation Category

TSC = Transport Service Category

TTW = Tank-to-Wheel/Wake

UIC = Union Internationale des Chemins de Fer (International Union of Railways)

UN = United Nations

UNGC = United Nations Global Compact

US EPA = United States Environmental Protection Agency

VLSFO = Very Low Sulfur Fuel Oil

WBCSD = World Business Council for Sustainable Development

WRI = World Resources Institute

WTT= Well-to-Tank

WTW = Well-to-Wheel/Wake

WWF = World Wildlife Fund for Nature

Settlement of solar power and wind power

Settlement of solar power and wind power from own installations.

Read more about the settlement of solar and wind here: The Danish Energy Agency

The EU aims to reduce CO2 emissions by 55% by 2030 compared to 1990

What are the EU's objectives?

By 2030, the EU aims to reduce CO2 emissions by 55% (compared to 1990)

The EU legislates on various matters and has in recent years incorporated considerations for the climate when legislating on other topics, such as housing construction and agricultural support, as well as in common regulations for vacuum cleaners, aviation, and much more. The EU has a special scheme for the 11,000 most climate-polluting companies. They are required to reduce their emissions by 43% (compared to 2005). Each country is also mandated to lower its CO2 emissions. In Denmark, we are required to reduce 39% of our CO2 emissions.

Additionally, the EU has adopted objectives for production and use of energy by 2030:

- The EU aims to increase the share of energy consumption in the EU from renewable sources such as solar, water, and wind to 27%.

- The EU aims to improve the efficiency of energy consumption by 27% (e.g., through better insulation of buildings).

EU's long-term goal is to strive to become the first climate-neutral continent by 2050.

Sources:

https://www.eu.dk/da/temaer/klima-og-groen-omstilling/eus-klimamaal

https://climate.ec.europa.eu/eu-action/climate-strategies-targets/2050-long-term-strategy_en

What is a Double Materiality Analysis, and Why is it Important for Your Company?

If your company is subject to CSRD reporting, you must conduct a double materiality assessment. But what does that actually mean?

A double materiality assessment determines which topics should be reported in your CSRD report and which can be omitted. This assessment evaluates topics based on two dimensions:

-

Financial Materiality: This dimension assesses how significant a given factor is for the company's financial performance. It focuses on identifying and reporting issues that could impact the company's finances, making them relevant for investors and other financial stakeholders.

-

Impact Materiality: This dimension evaluates the significance of the company’s activities regarding their impact on the environment, society, and people. It aims to identify and report the most critical social and environmental consequences of the company’s actions, regardless of their financial impact.

By combining these two dimensions, companies gain a holistic view of the topics most critical to their sustainability efforts.

How is the threshold value used in the assessment?

To structure the double materiality assessment, a scale from 1 to 5 is used to evaluate the importance of each topic. The total point value for each topic determines its placement in one of nine fields, allowing the company to identify and prioritize the most significant areas. This threshold value ensures that the most important topics, from both financial and sustainability perspectives, stand out clearly.

The company should consider its impacts in the short, medium, and long term, as their significance may change over time. Before starting the assessment, it is essential to have a thorough understanding of the business model and value chain, so that the relevant functions, suppliers, and partners can be involved in addressing sustainability issues.

Read more here:

Virksomhedsguiden (Business Guide made by The Danish Business Authority)

Dansk Industri (Confederation of Danish Industry)

What is an EPD & a PCR?

An Environmental Product Declaration (EPD) and a Product Category Rule (PCR) document are central elements in assessing a product's environmental performance. An EPD is a standardized document that transparently and comparably communicates the product’s environmental impact based on a Life Cycle Assessment (LCA). PCRs define the specific rules and guidelines used to prepare an EPD for a particular product category, ensuring that the reported data is relevant and consistent across similar products.

The purpose of both EPDs and PCRs is to enable stakeholders such as customers, architects, and regulators to understand and compare the environmental impact of different products in a uniform manner. While EPDs present key environmental data in an easily understandable format, PCRs ensure that the methods used are consistent and comply with standardized requirements, fostering reliable and sustainable choices.

Which standards do we refer to?

To ensure that our EPDs and PCRs are reliable and in compliance with international standards, we adhere to the following:

-

ISO 14025:2006: This standard establishes the principles and procedures for developing EPDs, including requirements for transparency, third-party verification, and the use of PCRs to ensure comparability between products.

-

EN 15804:2012+A2:2019: This standard specifies the requirements for EPDs for construction products and includes all relevant phases of the product’s lifecycle as well as the specific environmental indicators that must be reported.

By following these standards, we ensure that our EPDs and PCRs are accurate, verifiable, and can be used to make informed decisions about sustainability in line with best practices in environmental assessment.

If you have further questions about EPDs, PCRs, or our methods, please feel free to contact us.

How do we calculate CO2e reductions

How do we calculate CO2e reductions from internal recycling, and why do we use negative values?

In CEMS reduction calculator, we use emission factors from the Climate Compass to estimate CO2e reductions achieved by internal recycling of materials such as wood. When we recycle materials internally instead of buying new, we avoid the CO2e emissions that would otherwise be associated with the production of new materials. This avoided emission is represented as a negative value in our calculator, which clearly shows the real savings in CO2e emissions.

This calculation methodology is based on recognised principles, including Climate-KIC's Guidance on Avoided Emissions, which recommends documenting avoided emissions through recycling as part of a reliable and consistent decarbonisation strategy. Climate-KIC (Climate Knowledge and Innovation Communities) is one of the operational units of the EIT (European Institute of Innovation and Technology) working in the field of climate. EIT Climate-KIC is Europe's leading initiative in climate innovation, which works to accelerate the transition to a climate-neutral economy through education, entrepreneurship and cross-sector partnerships. It is a knowledge and innovation community supported by the EU that develops solutions to combat climate change. By combining the Climate Compass emission factors with this methodology, we ensure that our approach to quantifying CO2e reductions is both correct and based on best practice in the field.

Read more about the EIT here: https://eit.europa.eu/

Read more about Climate KIC here: https://www.climate-kic.org/

What is a GAP Analysis?

GAP stands for "Gap Analysis Process"

A GAP analysis is a systematic method used to identify the difference between a company's current performance and its desired goals or standards. The analysis helps uncover gaps between existing practices and requirements, such as those set by CSRD or ESRS. By understanding these gaps, the company can develop an action plan to close them and ensure that sustainability or compliance targets are met. A GAP analysis is therefore a valuable tool for improving efficiency and ensuring compliance with relevant standards.

CEMS Liability Insurance

CEMS Liability Insurance covers Commercial Liability, Product Liability, as well as Ingredient and Component coverage. The insurance also includes professional liability insurance for IT companies, Legal Assistance, and Cyber Insurance, which also covers online banking. The insurance is underwritten by IF Insurance under agreement number SP6362100.1.3.

The idea behind CEMS

Here’s the English translation of the revised description:

Lars Thomas Kristensen is the visionary behind CEMS – Climate ESG Monitoring System. He has over 20 years of experience in CO2e reporting and co-founded the social enterprise GOGGS Foundation (www.goggs.dk). Through GOGGS Foundation, Lars Thomas Kristensen has worked extensively with CSR and the "S" (Social) aspects of ESG for more than two decades.

Lars Thomas Kristensen also brings experience from serving on several boards, where he has gained significant insight and expertise in the "G" (Governance) aspects of ESG.

The development of CEMS began in 2019, driven by his extensive experience and vision to create an intuitive and comprehensive tool for sustainability reporting.

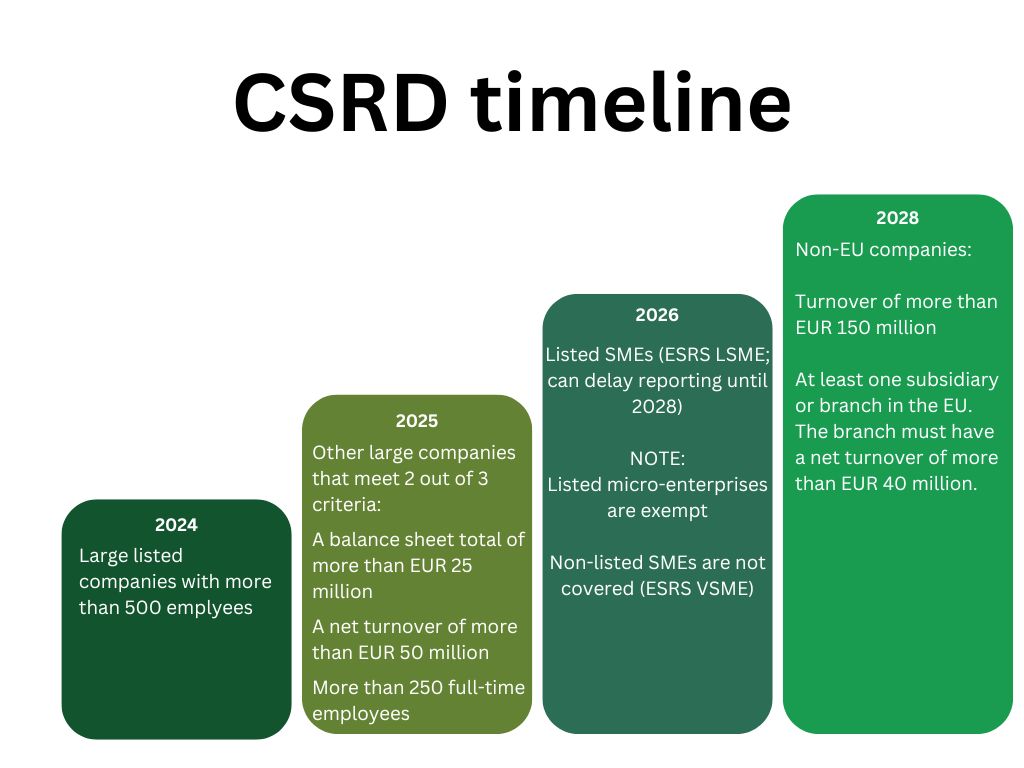

What is CSRD?

The CSRD is an EU directive that from 2024 requires large and listed companies to report on sustainability according to the ESRS standards. The rules will gradually cover more companies in the coming years.

The aim is to create consistency in sustainability reporting across the EU and increase transparency so that investors and stakeholders can more easily assess the sustainability of companies. It also helps companies document their sustainable efforts and avoid greenwashing in marketing.

- 2024: The sustainability reporting requirements will only apply to listed companies and state-owned limited companies with more than 500 employees from the financial year starting on or after 1 January 2024.

- 2025: Other large companies are covered by the requirements from the financial year starting 1 January 2025 or later, if they exceed two of these three criteria in two financial years:

- Balance sheet total over DKK 195 million

- Net sales DKK 391 million

- Over 250 full-time employees

- 2026: From the 2026 financial year, listed SMEs must report according to adapted standards, but can wait until 2028. Micro-enterprises are exempt. Non-listed SMEs are not covered, but a voluntary standard is expected for those who wish to report on sustainability.

Companies covered by the CSRD must publish significantly expanded and standardised information on sustainability that is more comprehensive than the requirements in section 99a of the Danish Financial Statements Act on corporate social responsibility. The reporting must include details on human rights, working conditions, management, and climate and environment. In addition, in the future, the auditor will have to provide a limited assurance opinion on sustainability reporting, as opposed to the previous requirement for a consistency check.

Souces:

Virksomhedsguiden (Business Guide made by The Danish Business Authority)

Erhvervsstyrelsen (The Danish Business Authority)

What is CS3D?

The upcoming EU directive CSDDD (Corporate Sustainability Due Diligence Directive) (CEMS will use the term CS3D in the future) will require certain companies to use due diligence processes to manage risks to people and the environment. The details of the requirements, who they apply to and when they will enter into force are still under negotiation in the EU.

It is unclear when the CS3D will enter into force, as the proposed directive is still being negotiated in the EU. If adopted in 2024, the requirements will apply from 2026 at the earliest, possibly later, and smaller companies may have more time to adapt.

CS3D requires certain companies to use due diligence processes to address negative impacts on people and the environment. The directive is expected to apply to larger EU companies as well as certain foreign companies in the EU. Although smaller companies are not directly covered, they may be affected as suppliers to larger companies and therefore face due diligence requirements. It is a good idea to prepare now.

CS3D requires companies to report annually on their due diligence efforts in the annual report according to specific standards. For companies that are not covered by the CSRD, the EU Commission will later determine the reporting requirements.

Companies will be monitored and may receive injunctions, bans, and fines for violations. Victims can also sue companies for damages if they have not conducted proper due diligence, with damages cases being settled in court.

Source: Virksomhedsguiden (Business Guide made by The Danish Business Authority)